So what do you do with RM 1,000?

Here's a good guide on growing your money in investing!

You may scoff at the idea of getting into investments with just RM1,000. You might think, “What can I do with that meagre amount?” A lot, actually. You’ll be surprised at how much you can gain in years to come if you invest that money right now.

You don’t need to invest hundreds of thousands up front to see a healthy return. With just RM1,000, you can kick-start your investment portfolio and see money rolling in.

According to your risk appetite, here’s an investment guide on where you can put your RM1,000 and see it grow.

Average return: 8% to 10% per annum

Example: If you invest RM1,000 over 10 years, your return will be RM1,367.36 excluding dividend and bonus

ASB is a premier unit trust investment specifically for Malaysian Bumiputera. It is managed by Amanah Saham Nasional Berhad (ASNB), a wholly-owned subsidiary of Permodalan Nasional Berhad (PNB).

It is meant as a long-term investment, with the longer you keep your money, the higher the possibility of higher return.

Some of the ASB features:

Average return: 6.82% per annum

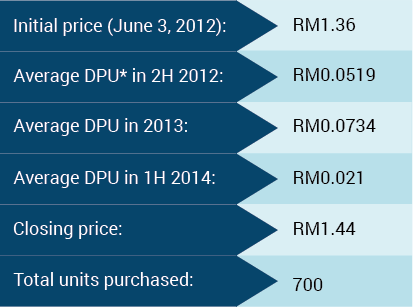

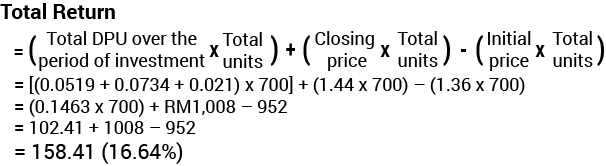

Example: If you purchased 700 shares from Sunway REITs in 2012, and sold them in the first quarter of 2014:

REITs are meant for investors who would like to invest in property, especially retail lots, but do not have the capital to buy them outright as investments. These trusts are formed by companies that purchase and manage real estate using funds pooled from shareholders. Dividend payouts can be generous depending on which REIT you are buying.

Like most long-term investments, the longer you leave your money in it, the higher the return will most likely be.

* DPU stands for Distribution Per Unit, or also known as, dividend per share of the financial year. It is listed in sen.

Return: Depends on portfolio and funds

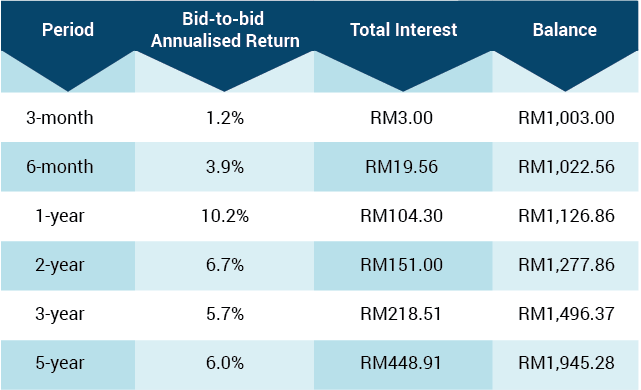

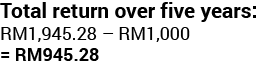

Example: If you invest RM1,000 in the AMB Lifestyle Trust Fund Today for five years on Fundsupermart.com.my, your return, based on the historical performance, may be:

Unit trust funds are a form of collective investment that allows investors with similar investment objectives to pool their funds to be invested in a portfolio of securities or other assets. A professional fund manager then invests the pooled funds in a portfolio which may include cash, bonds and deposits, shares, properties and/or commodities.

The return on investment of unit holders is usually in the form of income distribution and capital appreciation, derived from the pool of assets supporting the unit trust fund. Each unit earns an equal return, determined by the level of distribution and/or capital appreciation in any one period.

However, investing in unit trust will usually involve certain costs like sales charge, platform fee, annual management charge, trustee fee and other charges. By investing via Fundsupermart, investors can reduce these fees and charges as compared to investing through a fund manager.

With a unit trust fund, you can still maintain liquidity and security, but it is no longer a savings account – it is an investment. Unit trust is the most suitable investment for the common man who is interested in equities but lack the funds to diversify independently. Unit trusts offers an opportunity to invest in a diversified, professionally managed portfolio with lower starting capital.

Compare the performance of different funds to find the best one to invest on using our unit trust comparison page.

Return: Possibly high return, depending on market and company

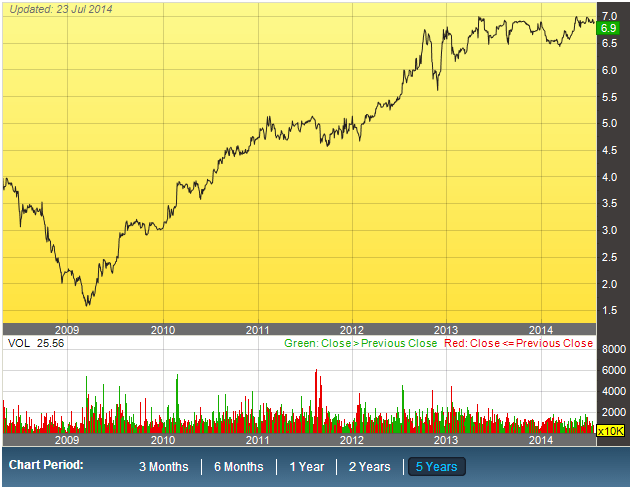

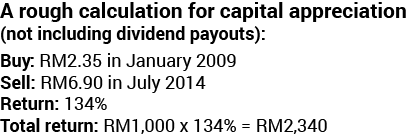

Example: If you invested RM 1,000 in Axiata in 2009 (five years ago), it would amount to about RM2,340 now.

Investing in blue chip stocks are recommended not just because of the capital appreciation, but also the attractive dividends, depending on the company. In the example above, Axiata is a well-known and reputable blue chip company.

Blue chip companies refer to reputable and financially sound companies, selling high-quality, and widely accepted products and services. These companies are known to weather downturns and operate profitably in the face of adverse economic conditions, which helps to contribute to their long record of stable and reliable growth.

However, if you’re risk averse and not well informed, stocks should not be used as a short-term investment in order to make a big profit. This action is not investing, but pure gambling. There may be times in which stocks have put a record on short-term growth, but these occurrences are very rare.

Making short-term transactions with stocks can lead to high cost of investment due to the various brokerage and transaction fees. Depending on your investment amount, these fees can add up to a significant amount.

As Warren Buffett once said, “If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.”

No matter which investment vehicle you pick, it should have a long-term flavour. That way, you don’t get eaten alive by trading fees on a relatively small amount of money invested, and there can potentially be higher return on your money.

For most people who are struggling to save up on some money to invest, remember, it can always be done over time. You can always top up your investment in various investment vehicles as and when you have saved up some investment fund. If you keep at it over time you will gradually build up a pretty secure and diverse investment portfolio. It’s always good to start early!

SOURCE

Here's a good guide on growing your money in investing!

Investment Guide: You Have RM1,000. Now Where Do You Invest It?

You may scoff at the idea of getting into investments with just RM1,000. You might think, “What can I do with that meagre amount?” A lot, actually. You’ll be surprised at how much you can gain in years to come if you invest that money right now.

You don’t need to invest hundreds of thousands up front to see a healthy return. With just RM1,000, you can kick-start your investment portfolio and see money rolling in.

According to your risk appetite, here’s an investment guide on where you can put your RM1,000 and see it grow.

Amanah Saham Bumiputera (ASB)

Risk: LowAverage return: 8% to 10% per annum

Example: If you invest RM1,000 over 10 years, your return will be RM1,367.36 excluding dividend and bonus

ASB is a premier unit trust investment specifically for Malaysian Bumiputera. It is managed by Amanah Saham Nasional Berhad (ASNB), a wholly-owned subsidiary of Permodalan Nasional Berhad (PNB).

It is meant as a long-term investment, with the longer you keep your money, the higher the possibility of higher return.

Some of the ASB features:

- Capital guaranteed – low risk

- No sales charges – higher return

- No redemption charges – higher return

- Maximum investment amount: 200,000 units

Real Estate Investment Trusts (REITs)

Risk: MediumAverage return: 6.82% per annum

Example: If you purchased 700 shares from Sunway REITs in 2012, and sold them in the first quarter of 2014:

REITs are meant for investors who would like to invest in property, especially retail lots, but do not have the capital to buy them outright as investments. These trusts are formed by companies that purchase and manage real estate using funds pooled from shareholders. Dividend payouts can be generous depending on which REIT you are buying.

Like most long-term investments, the longer you leave your money in it, the higher the return will most likely be.

* DPU stands for Distribution Per Unit, or also known as, dividend per share of the financial year. It is listed in sen.

Unit trust funds

Risk: Low to mediumReturn: Depends on portfolio and funds

Example: If you invest RM1,000 in the AMB Lifestyle Trust Fund Today for five years on Fundsupermart.com.my, your return, based on the historical performance, may be:

Performance figures (as of July 22, 2014)

Unit trust funds are a form of collective investment that allows investors with similar investment objectives to pool their funds to be invested in a portfolio of securities or other assets. A professional fund manager then invests the pooled funds in a portfolio which may include cash, bonds and deposits, shares, properties and/or commodities.

The return on investment of unit holders is usually in the form of income distribution and capital appreciation, derived from the pool of assets supporting the unit trust fund. Each unit earns an equal return, determined by the level of distribution and/or capital appreciation in any one period.

However, investing in unit trust will usually involve certain costs like sales charge, platform fee, annual management charge, trustee fee and other charges. By investing via Fundsupermart, investors can reduce these fees and charges as compared to investing through a fund manager.

With a unit trust fund, you can still maintain liquidity and security, but it is no longer a savings account – it is an investment. Unit trust is the most suitable investment for the common man who is interested in equities but lack the funds to diversify independently. Unit trusts offers an opportunity to invest in a diversified, professionally managed portfolio with lower starting capital.

Compare the performance of different funds to find the best one to invest on using our unit trust comparison page.

Blue chip stocks in Stock Exhange

Risk: HighReturn: Possibly high return, depending on market and company

Example: If you invested RM 1,000 in Axiata in 2009 (five years ago), it would amount to about RM2,340 now.

AXIATA 5 Years Source: Bursa Malaysia

Investing in blue chip stocks are recommended not just because of the capital appreciation, but also the attractive dividends, depending on the company. In the example above, Axiata is a well-known and reputable blue chip company.

Blue chip companies refer to reputable and financially sound companies, selling high-quality, and widely accepted products and services. These companies are known to weather downturns and operate profitably in the face of adverse economic conditions, which helps to contribute to their long record of stable and reliable growth.

However, if you’re risk averse and not well informed, stocks should not be used as a short-term investment in order to make a big profit. This action is not investing, but pure gambling. There may be times in which stocks have put a record on short-term growth, but these occurrences are very rare.

Making short-term transactions with stocks can lead to high cost of investment due to the various brokerage and transaction fees. Depending on your investment amount, these fees can add up to a significant amount.

As Warren Buffett once said, “If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.”

No matter which investment vehicle you pick, it should have a long-term flavour. That way, you don’t get eaten alive by trading fees on a relatively small amount of money invested, and there can potentially be higher return on your money.

For most people who are struggling to save up on some money to invest, remember, it can always be done over time. You can always top up your investment in various investment vehicles as and when you have saved up some investment fund. If you keep at it over time you will gradually build up a pretty secure and diverse investment portfolio. It’s always good to start early!

SOURCE